Accounting and Reporting for Emissions Under Scope 2

Methods for calculating and reporting scope 2 emissions have a significant impact on how a company evaluates its performance and which mitigation actions are encouraged. As per Corporate Standard multiplying activity data (MWhs of electricity consumption) by source- and supplier-specific emission factors to determine the total GHG emissions impact of electricity consumption. In addition, it emphasizes the function of green power programs in reducing emissions from electricity consumption. Companies are advised to use statistics such as local or national grid emission factors only if these forms of information about electricity supply are unavailable.

Different approaches for calculating Scope 2 emissions on the basis of energy sources:-

Location-based method:

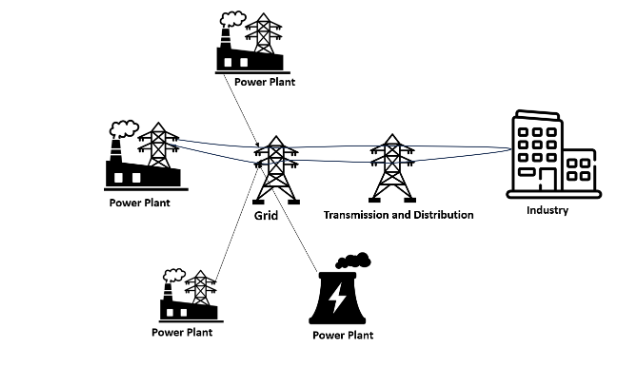

This is known as the location-based strategy if Company A buys electricity from the local grid. Various power plants supplied energy to the local grid which have different emission factors. Currently, business A want to disclose its carbon emissions for Scope 2, but it’s unclear what the precise emission factor for the power they consumed . The industry is unaware of the specific power plant that supplied the electricity. For the purpose of calculating emissions, the industry is forced to depend on average emission factors. Company A must purchase energy from a source that can give them precise emission factors and compute the emission factor for calculation if they wish to lower their Scope 2 emissions.

The location-based method is based on aggregated and averaged statistical emission data and electricity output within a defined geographic boundary and over a defined time period. The location-based approach takes the average emission factors of the power systems into account.

- Regional Emission Factor – These are the average emission factors for baseload, intermediate, and peaking units of all plants that produce energy for the grid.

- National Emission Factor– published by national governments or by the International Energy Agency (IEA).

Market-based method:

The market-based approach takes into account the GHG emissions associated with a consumer’s option of electricity supplier or product. These options, such as selecting a retail electricity supplier, a particular generator, a differentiated electricity product, or the purchase of unbundled energy attribute certificates, are communicated through contracts between the purchaser and the provider. An energy user uses the greenhouse gas emission factor linked to its ownership of qualifying contractual instruments under the market-based technique of scope 2 accounting.

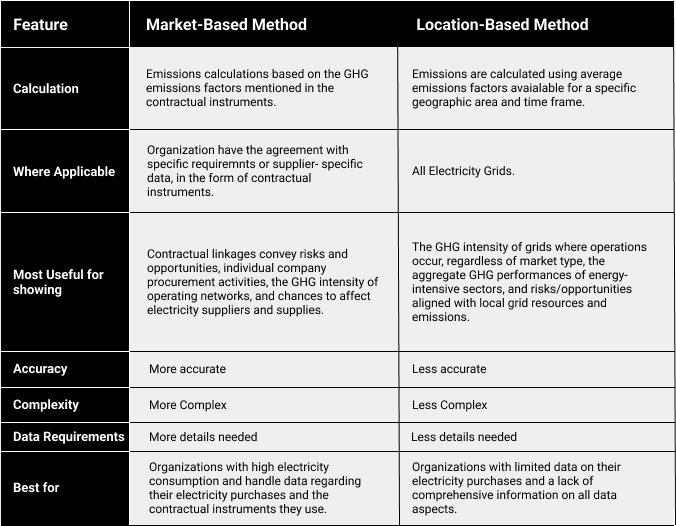

Difference between Market Based & Location Based :-